Long Call Butterfly

Introduction

Based on your research, you believe the stock you are interested in is going to trade within a narrow range in the future. However, you are not confident about the direction of the potential moves, and it is important to you that your risks are limited. You are looking to express your opinion that the stock’s volatility will decrease and are familiar with call positions and advanced options strategies.

Utilizing your foundational knowledge of call positions, you decide to establish two call spread positions.

What exactly is a Long Call Butterfly?

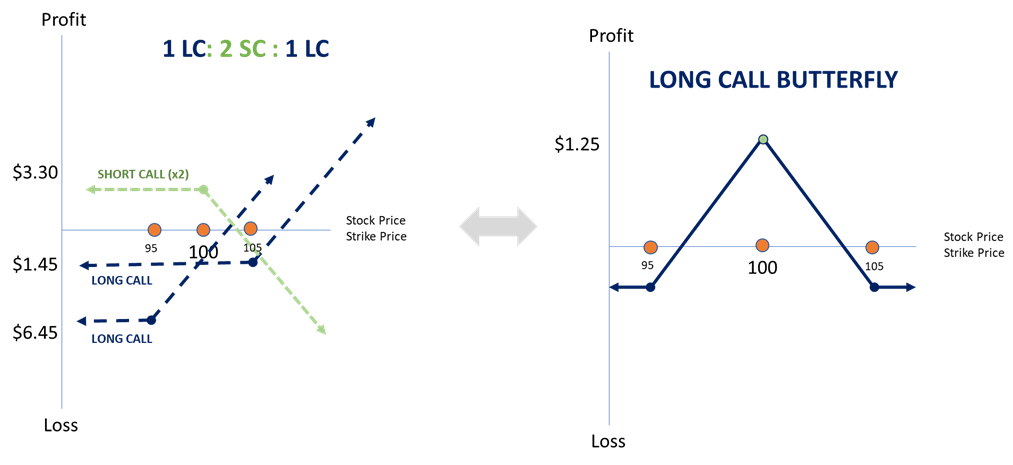

A long butterfly spread with calls is a three-part strategy created by:

- buying one call at a lower strike price,

- selling two calls with a higher strike price, and

- buying one call with an even higher strike price.

All calls have the same expiration date, and the strike prices are equidistant.

This strategy is established for a net debit, and both the potential profit and maximum risk are limited.

The maximum profit is realized if the stock price is equal to the strike price of the short calls (center strike) on the expiration date.

The maximum risk is the net cost of the strategy including commissions and fees. This maximum loss occurs if the stock price is above the highest strike price or below the lowest strike price at expiration.

The long call butterfly is considered an advanced strategy because the profit potential is small in dollar terms while “costs” are high. Given that there are three strike prices, there may be significant commissions and fees.

Curious why it’s called a “butterfly?” The term “butterfly” in the strategy name is thought to have originated from the shape of the profit-loss diagram at expiration. The peak in the middle of the diagram of a long butterfly spread looks vaguely like the body of a butterfly, and the horizontal lines stretching out above the highest strike and below the lowest strike look vaguely like its wings.

A long butterfly spread with calls can also be described as the combination of a bull call spread and a bear call spread. The bull call spread is long the lowest-strike call combined with a short center-strike call, while the bear call spread combines the other short center-strike call with a long position in the highest-strike call.

Long Call Butterfly Strategy: Additional Observations

A long call butterfly spread may be the strategy of choice when the forecast is for stock price action near the center strike price of the spread because long butterfly spreads profit from time decay. However, unlike a short straddle or short strangle, the potential risk of a long butterfly spread is limited. The tradeoff for this limited risk is that a long butterfly spread has a much lower profit potential in dollar terms than a comparable short straddle or short strangle. Also, the commissions for a butterfly spread are higher than those for a straddle or strangle.

Long butterfly spreads are sensitive to changes in volatility. The net price of a butterfly spread falls when volatility rises and rises when volatility falls. Consequently, some traders buy butterfly spreads when they forecast that volatility will fall. Since the volatility in option prices may fall after earnings reports, some traders may choose to implement a long butterfly spread immediately before the report. The potential profit is “high” in percentage terms and risk is limited to the cost of the position including commissions. For the strategy to be profitable, it requires that the stock price stay between the lower and upper strike prices of the butterfly. If the stock price rises or falls too much, then losses may be incurred.

If volatility is constant, long call butterfly spreads do not rise in value and, therefore, do not show much of a profit until they are very close to expiration and the stock price is close to the center strike price. In contrast, short straddles and short strangles begin to show at least some profit early in the expiration cycle if the stock price does not move out of the profit range.

Furthermore, while the potential profit of a long butterfly spread is considered a “high percentage profit on the capital at risk,” the typical dollar cost of one butterfly spread is “low.” As a result, it is often necessary to trade many butterfly spreads if the goal is to earn a profit in dollars equal to the desired dollar profit from a short straddle or strangle. Also, it is important to keep in mind that the risk of a long butterfly spread is still the full net premium paid to establish the position.

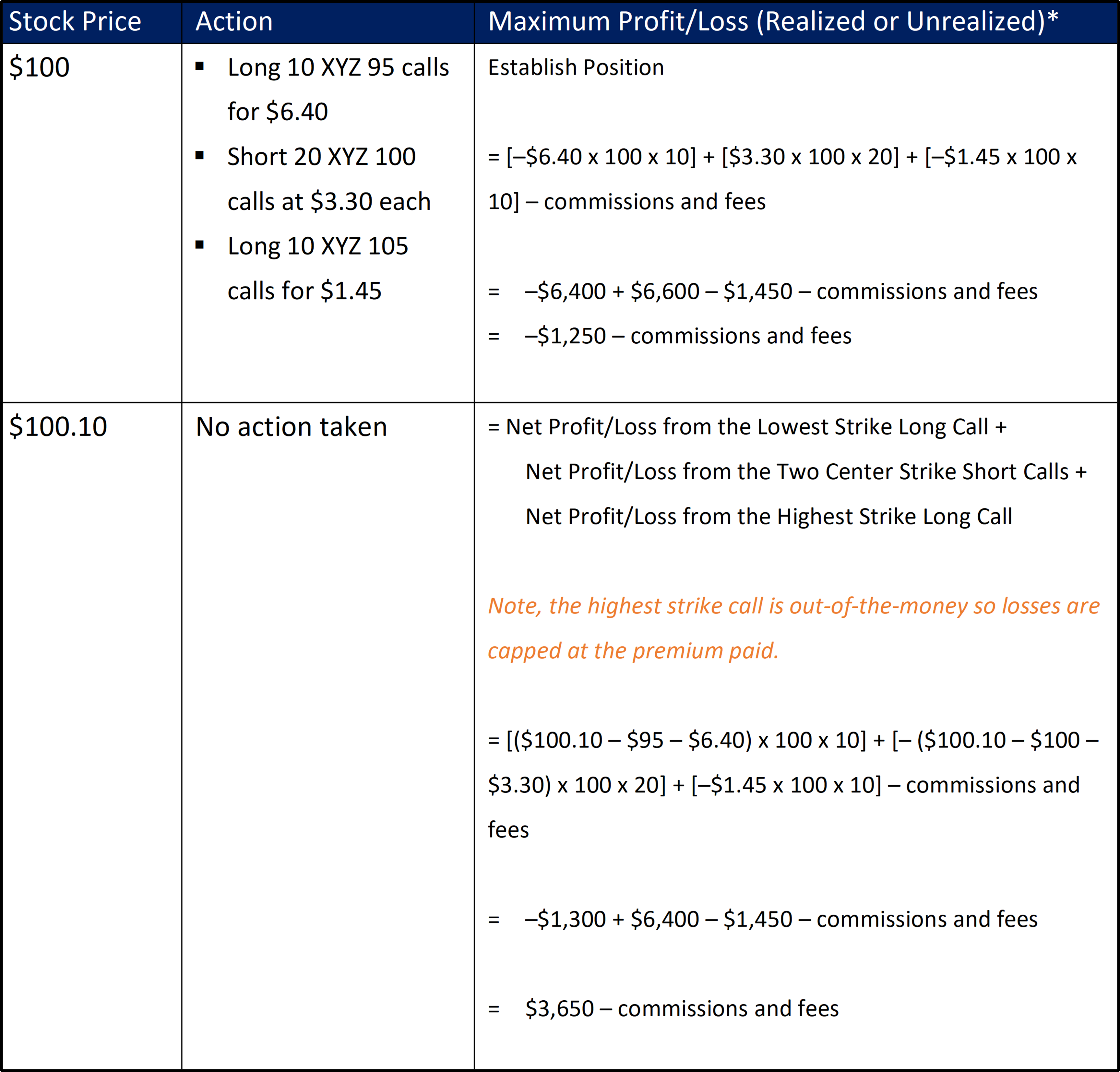

Example

- Long 10 XYZ January 95 calls for $6.40

- Short 20 XYZ January 100 calls at $3.30 each

- Long 10 XYZ January 105 calls for $1.45

In our example, assume stock XYZ is currently trading at $100, and we establish a long call butterfly position.

We buy 10 XYZ January 95 calls for a total of $6,400 (10 x 100 multiplier x $6.40), sell 20 XYZ January 100 calls for a total of $6,600 (20 x 100 multiplier x $3.30), and buy 10 XYZ January 105 calls for $1,450 (10 x 100 multiplier x $1.45) plus transaction fees and commissions.

As a result of these simultaneous trades, our account has a debit balance of approximately $1,250 (excluding transaction fees and commissions).

Outcome 1: Profit

With a long call butterfly position, we believe volatility will decrease. This means our sentiment is neutral, believing that the stock price will trade near the middle strike price at expiration.

Assume we are correct in our sentiment and the stock price remains unchanged.

To calculate our profit at expiration on the long call butterfly position, simply sum the profit or loss of the individual legs of the trade using the following formula:

Net Profit = Net Profit/Loss from the Lowest Strike Long Call + Net Profit/Loss from the Two Center Strike Short Calls + Net Profit/Loss from the Highest Strike Long Call

Recall the formulas for calculating the profit/loss on an individual call option:

If S – K > 0,

Long Call Profit = Current Stock Price – Strike Price – Net Premium Paid

Short Call Loss = – (Current Stock Price – Strike Price – Net Premium Received)

If S – K < 0,

Short Call Profit = Net Premium Received

Long Call Loss = Net Premium Paid

Max Profit = Center Strike – Lowest Strike – Net Premium Paid

Example

Stock XYZ is trading at $100 and you establish a long call butterfly position.

- Long 10 XYZ January 95 calls for $6.40

- Short 20 XYZ January 100 calls at $3.30 each

- Long 10 XYZ January 105 calls for $1.45

A week later, stock XYZ is trading at $100.10

*Unrealized profits are those that potentially exist; realized profits/losses occur when you close out or trade out of the position.

Outcome 2: Loss

Let’s assume the market had a major move down and we are incorrect about our volatility forecast. To calculate our loss on the position, use the following formula:

Loss = Net Profit/Loss from the Lowest Strike Long Call + Net Profit/Loss from the Two Center Strike Short Calls + Net Profit/Loss from the Highest Strike Long Call

Max Loss = Total Premium Paid

Example

Stock XYZ is trading at $100 and you establish a long call butterfly position.

- Long 10 XYZ January 95 calls for $6.40

- Short 20 XYZ January 100 calls at $3.30 each

- Long 10 XYZ January 105 calls for $1.45

A week later, stock XYZ is trading down at $90.

*Unrealized profits are those that potentially exist; realized profits/losses occur when you close out or trade out of the position.

Outcome 3: Breakeven

There are two potential breakeven points for the long call butterfly:

- Lowest strike plus net premium paid

- Highest strike minus net premium paid

Lower Breakeven Price = Lowest Strike Price + Net Premium Paid

Upper Breakeven Price = Highest Strike Price – Net Premium Paid

Example

Stock XYZ is trading at $100, and you establish a long call butterfly position.

· Long 10 XYZ January 95 calls for $6.40

· Short 20 XYZ January 100 calls at $3.30 each

· Long 10 XYZ January 105 calls for $1.45

· Fees and commissions = $20 total or $0.20 per share

Lower Breakeven Price = $95 + $1.25 + $0.20 = $96.45

Upper Breakeven Price = $105 – $1.25 – $0.20 = $103.55

At-A-Glance

Strategy

Long Call Butterfly

Alternative Name

n/a

Pre-Requisite Strategy Knowledge

Long Call

Short Call

Bear Call Spread

Bull Call Spread

Legs of Trade

3 legs

Sentiment

Neutral

Example

· Long 10 XYZ January 95 calls

· Short 20 XYZ January 100 calls

· Long 10 XYZ January 105 calls

Rule to Remember

The intervals between the strike prices of the three positions must be equal and in ascending order. The total quantity of the long calls must equal the quantity of the short calls.

Max Potential Profit (GAIN)

Limited to difference between center strike and lowest strike less net premium paid

Break-Even Points

At expiration, there are two potential breakeven points:

§ Lower breakeven = Lowest strike plus total premium paid for the butterfly

§ Upper breakeven = Highest strike less total premium paid for the butterfly

Max Potential Risk (LOSS)

Total premium paid plus transaction fees and commissions

Ideal Outcome

XYZ price trades at or near the middle strike price at expiration

Early Assignment Risk

Equity options in the United States can be exercised on any business day, and the holder of a short options position has no control over when they will be required to fulfill the obligation. Therefore, the risk of early assignment must be considered when entering positions involving short options. Early assignment of options is generally related to dividends, and short calls that are assigned early are generally assigned on the day before the ex-dividend date. In-the-money calls whose time value is less than the dividend have a high likelihood of being assigned, whereas in-the-money puts whose time value is less than the dividend have a high likelihood of being assigned.

The long calls in a long butterfly spread have no risk of early assignment.

The short calls do have such risk.

If one short call is assigned, then 100 shares of stock are sold short and the long calls (with the lowest and highest strike prices) remain open. If a short stock position is not wanted, it can be closed in one of two ways. First, 100 shares can be purchased in the marketplace. Second, the short 100-share position can be closed by exercising the long call with the lowest strike.

Remember, however, that exercising a long call will forfeit the time value of that call. Therefore, it is generally preferable to buy shares to close the short stock position and then sell the long call. This two-part action recovers the time value of the long call. One caveat is commissions. Buying shares to cover the short stock position and then selling the long call is only advantageous if the commissions are less than the time value of the long call.

If both of the short calls are assigned, then 200 shares of stock are sold short and the long calls (with the lowest and highest strike prices) remain open. Again, if a short stock position is not wanted, it can be closed in one of two ways. Either 200 shares can be purchased in the marketplace, or both long calls can be exercised. However, as discussed above, since exercising a long call forfeits its time value, it is generally preferable to buy shares to close the short stock position and then sell the long calls. The caveat, as mentioned above, is commissions. Buying shares to cover the short stock position and then selling the long calls is only advantageous if the commissions are less than the time value of the long calls.

Note, however, that whichever method is used (buying stock and selling the long call or exercising the long call), the date of the stock purchase will be one day later than the date of the short sale. This difference will result in additional fees, including interest charges and commissions. Assignment of a short option might also trigger a margin call if there is not sufficient account equity to support the stock position created.

Potential Position Created at Expiration:

The position at expiration of a long butterfly spread with calls depends on the relationship of the stock price to the strike prices of the spread:

- If the stock price is below the lowest strike price, then all calls expire worthless, and no position is created.

- If the stock price is above the lowest strike and at or below the center strike, then the lowest strike long call is exercised. The result is that 100 shares of stock are purchased and a long stock position of 100 shares is created.

- If the stock price is above the center strike and at or below the highest strike, then the lowest-strike long call is exercised and the two middle-strike short calls are assigned. The result is that 100 shares are purchased, and 200 shares are sold. The net result is a short position of 100 shares.

- If the stock price is above the highest strike, then both long calls (with the lowest and highest strikes) are exercised and the two short calls (with the middle strike) are assigned. The result is that 200 shares are purchased, and 200 shares are sold. The net result is no position, although several stock buying and selling commissions have been incurred.

Charts

-Powered by The Options Institute