Covered Strangle

Introduction

Based on your research, you believe the stock you own is going to experience some modestly bullish moves in the future and you are looking to generate some income.

Utilizing your foundational knowledge of long call and long put positions, you decide to sell both.

What exactly is a Covered Strangle?

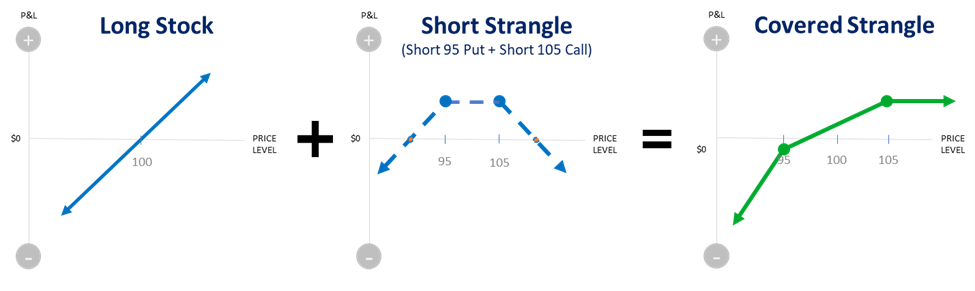

A covered strangle position is created by buying (or owning) stock and selling both an out-of-the-money call and an out-of-the-money put. The call and put have the same expiration date.

Note that the short put is not“covered” as the strategy name implies, because cash is not held in reserve to buy additional shares.

This strategy exposes you to the risks and benefits of short options. In this strategy you have significant downside risk because you have the exposure from your stock position as well as the short put. If the underlying stock declines sharply in price, both positions experience losses.

Example

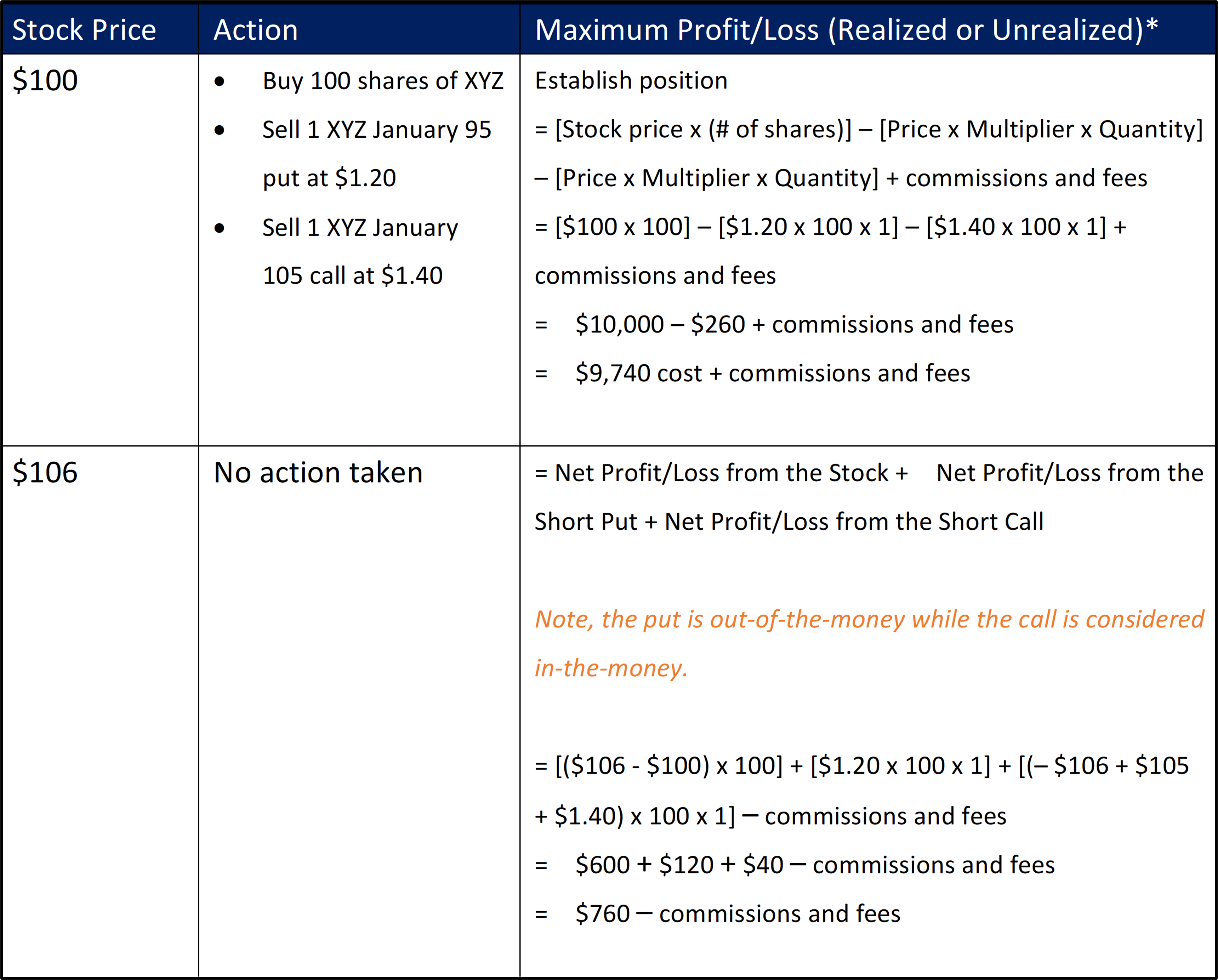

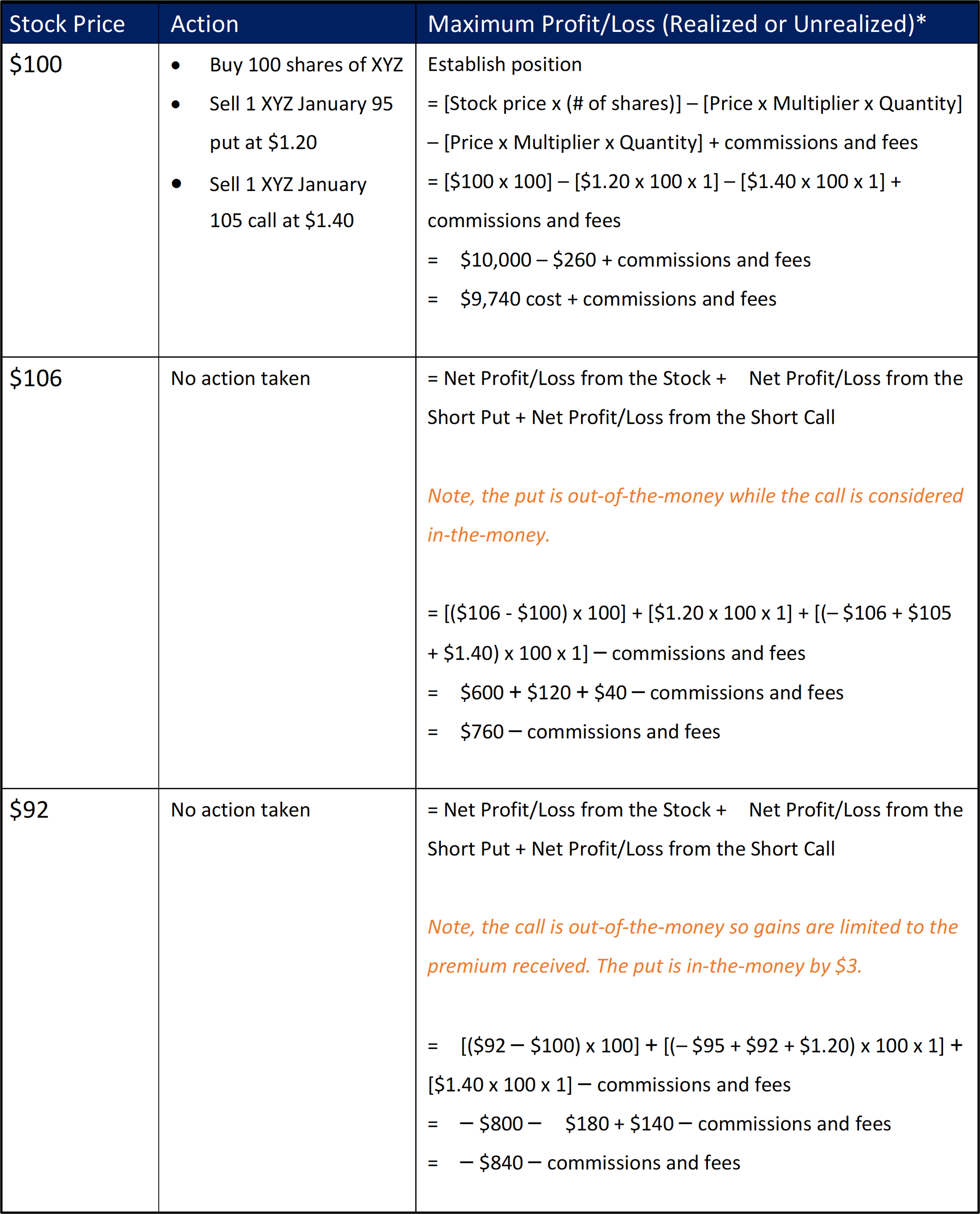

Buy 100 shares of XYZ for $100 per share

Sell 1 XYZ January 95 put at $1.20

Sell 1 XYZ January 105 call at $1.40

In our example, assume stock XYZ is currently trading at $100. We purchase 100 XYZ shares for a total of $10,000 (100 x $100), plus transaction fees and commissions. We sell 1 XYZ January 95 put for a total of $120 (1 x 100 multiplier x $1.20), less commissions and fees, and simultaneously sell 1 XYZ January 105 call for a total of $140 (1 x 100 multiplier x $1.40), less commissions and fees.

As a result of these three simultaneous trades, our account has a debit balance of approximately $9,740 (excluding commissions and fees).

Outcome 1: Profit

Let’s assume we are correct in our sentiment, and the stock price rises sharply. To calculate our profit at expiration on the position, use the following formula:

Profit = Net Profit/Loss from Long Stock + Net Profit/Loss from the Short Put + Net Profit/Loss from the Short Call

For the Long Stock,

Profit = Current Price – Original Purchase Price

For the Short Call,

if S – K > 0, then the Loss = – (Current Stock Price – Strike Price) + Net Premium Received

= – Current Stock Price + Strike Price + Net Premium Received

if S – K < 0, then the Profit = Net Premium Received

For the Short Put,

if K – S > 0, then the Loss = – (Strike Price – Current Stock Price) + Net Premium Received

= – Strike Price + Current Stock Price + Net Premium Received

if K – S < 0, then the Profit = Net Premium Received

The maximum profit is realized if the stock price is at or above the strike price of the short call at expiration. The overall profit potential is limited while the loss potential is significant if the stock price falls. Below the strike price of the put, losses are $2.00 per share for each $1.00 decline in stock price, because both the long stock and the short put create losses as the stock price declines.

Max Profit = Call Strike Price – Stock Price + Total Net Premiums Received

Example

Stock XYZ is trading at $100 and you establish a covered strangle position.

- Buy 100 shares of XYZ

- Sell 1 XYZ January 95 put at $1.20

- Sell 1 XYZ January 105 call at $1.40

A week later, stock XYZ is trading higher at $106.

*Unrealized profits/losses are those that potentially exist; realized profits/losses occur when you close out or trade out of the position.

Outcome 2: Loss

Let’s assume we are incorrect and the market declines sharply instead. To calculate our loss on the position, use the following formula:

Loss = Net Profit/Loss from the Long Stock + Net Profit/Loss from the Short Put + Net Profit/Loss from the Short Call

For the Long Stock,

Loss = Original Purchase Price – Current Stock Price

For the Short Call,

if S – K > 0, then the Loss = – (Current Stock Price – Strike Price) + Net Premium Received

= – Current Stock Price + Strike Price + Net Premium Received

if S – K < 0, then the Profit = Net Premium Received

For the Short Put,

if K – S > 0, then the Loss = – (Strike Price – Current Stock Price) + Net Premium Received

= – Strike Price + Current Stock Price + Net Premium Received

if K – S < 0, then the Profit = Net Premium Received

Max Loss = Potential loss is substantial and leveraged if the stock price falls. Below the lower strike price at expiration, losses are $2.00 per share for each $1.00 decline in stock price, because both the long stock and the short put lose as the stock price declines.

Example

Stock XYZ is trading at $100 and you establish a covered strangle position.

- Buy 100 shares of XYZ

- Sell 1 XYZ January 95 put at $1.20

- Sell 1 XYZ January 105 call at $1.40

A week later, stock XYZ is trading lower at $92.

*Unrealized profits/losses are those that potentially exist; realized profits/losses occur when you close out or trade out of the position.

Outcome 3: Breakeven

If Stock Price – Lower Strike Price > Total Net Premiums Received:

Breakeven = Stock Price – Total Net Premiums Received

If Stock Price – Lower Strike Price < Total Net Premiums Received:

Breakeven = Lower Strike Price – 0.50 x [Total Net Premiums Received – Stock Price + Lower Strike Price]

Example

Stock XYZ is trading at $100 and you establish a covered strangle position.

- Buy 100 shares of XYZ

- Sell 1 XYZ January 95 put at $1.20

- Sell 1 XYZ January 105 call at $1.40

In this example with the stock trading at $100,

Stock Price – Lower Strike Price = $100 – $95 = $5,

which is greater than the total net premiums received ($1.20 + $1.40 = $2.60). Therefore,

Breakeven = $100 – ($1.20 + $1.40) = $97.40

At-A-Glance

Strategy

Covered Strangle

Alternative Name

n/a

Pre-Requisite Strategy Knowledge

Long Stock

Short Call

Short Put

Short Strangle

Legs of Trade

3 legs

Sentiment

Moderately bullish

Example

- Buy 100 shares of XYZ for $100 per share

- Sell 1 XYZ January 95 put at $1.20

- Sell 1 XYZ January 105 call at $1.40

Rule to Remember

The short put and short call must have the same underlying and expirations, but different strikes (higher call strike, lower put strike).

Max Potential Profit (GAIN)

Call Strike Price – Stock Purchase Price + Total Net Premiums Received for Strangle

Break-Even Points

If Stock Price – Lower Strike Price > Total Net Premiums Received:

Breakeven = Stock Price – Total Net Premiums Received

If Stock Price – Lower Strike Price < Total Net Premiums Received:

Breakeven= Lower Strike Price – 0.50 x [Total Net Premiums Received – Stock Price + Lower Strike Price]

Max Potential Risk (LOSS)

Stock Purchase Price + Put Strike Price – Total Net Premiums Received for Strangle

Ideal Outcome

XYZ price rises far above the higher strike price. Note, significant losses are possible if the stock price declines.

Early Assignment Risk

Equity options in the United States can be exercised on any business day, and the holder of a short stock options position has no control over when they will be required to fulfill the obligation. Therefore, the risk of early assignment must be considered when entering positions involving short options.

Both the short call and the short put in a covered strangle have early assignment risk. Early assignment of stock options is generally related to dividends.

Short calls that are assigned early are generally assigned on the day before the ex-dividend date. In-the-money calls whose time value is less than the dividend have a high likelihood of being assigned. Therefore, if the stock price is above the strike price of the short call, an assessment must be made if early assignment is likely. In the case of a covered strangle, it is assumed that being assigned on the short call is a good event, because assignment of the call converts the stock position to cash and a profit is realized (not including the short put which remains open – with risk – until expiration). However, if selling the stock is not wanted, then buying the short call to eliminate the possibility of assignment is necessary.

Short puts that are assigned early are generally assigned on the ex-dividend date. In-the-money puts whose time value is less than the dividend have a high likelihood of being assigned. Therefore, if the stock price is below the strike price of the short put, an assessment must be made if early assignment is likely. In the case of a covered strangle, it is assumed that being assigned on the short put is not wanted, because the purchase of additional shares requires additional capital and/or a possible margin call. Therefore, if early assignment of the short put is deemed likely, the short put must be purchased to eliminate the possibility of assignment. However, if additional shares are wanted, then no action needs to be taken.

If early assignment of the short put does occur, and if the stock position is not wanted, the stock can be closed in the marketplace by selling. Note, however, that the date of the closing stock sale will be one day later than the date of the opening stock purchase (from assignment of the put). This one-day difference may result in additional fees, including interest charges and commissions. Assignment of a short put might also trigger a margin call if there is not sufficient account equity to support the stock position.

Potential Position Created at Expiration

If the short call in a covered strangle is assigned, then the stock is sold at the strike price of the call and replaced with cash. Assuming the put expires, there is no stock position, only cash.

If the short put in a covered strangle is assigned, then stock is purchased at the strike price of the put. Assuming the call expires, the result is that the initial stock position is doubled.

Charts